There have been a number of articles stating that the number of sales agreed on properties that subsequently fall through are rising, and that many properties are now being sold multiple times, as a result.

However, TwentyCi has conducted research into what they believe is happening in the housing market.

Why might more agreed sales on properties be falling through?

In June 2022, it was observed the amount of time it takes to buy a property was increasing, again. The average time to buy a property in the UK currently stands at an unprecedented 144 days (or 4.7 months).

Reasons have been presented for this in previous articles, such as the RICS Residential Market Survey, which argued this is related to low supply which prevents chains from forming as fast as they used to.

It has also been reported that in the sub £200k properties, stock has halved since pre-pandemic levels.

However, the 144 days it takes to buy a property today was only 88 days in June 2021, and a more realistic – because of the stamp duty effects – 93 days in June 2019. So, since June 2019 it now, potentially, takes a buyer 56% longer to buy a property than it did pre-pandemic. Consequently, more time could mean a greater risk of sales falling through.

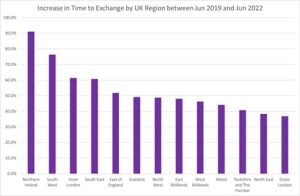

The time to buy a property can vary by UK region and price band. This first graph plots the increase in the time to buy a property by UK region comparing now to pre-pandemic:

This shows that the times to buy property have increased in all regions of the UK.

Northern Ireland and the South West have been disproportionately affected. In Northern Ireland, the length of time to buy a property has shot up from 120 days to 229. In the South West, the length of time to buy a property has shot up from 96 days to 169.

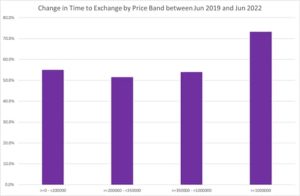

The next chart examines the change in time to buy, cutting the data by price band:

This shows that the most affected are the higher-priced properties over £1m, where it now takes 5.2 months to buy a property.

Are the number of property sales falling through increasing?

At a national level, in June 2019, 21% of properties with a sale agreed had at least one fallen through occurrence. In June 2022, this has moved to 21.1%. Therefore, according to these figures, the percentage of properties falling through has barely risen when compared with pre-pandemic levels.

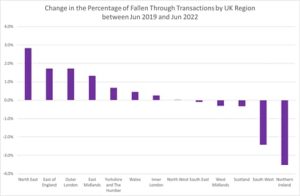

Looking at a national level, however, shows a different story. The following chart plots the change in the percentage of fallen through transactions by UK region between June 2019 and June 2022:

From this, we can observe that sales falling through are rising in the North East, the East of England, Outer London and the East Midlands. More importantly, however, we see that the percentage of sales falling through has declined dramatically in the South West and Northern Ireland. What this suggests is that even though it takes the longest amount of time to buy property in these two UK regions, their fallen through rates have actually fallen.

In Northern Ireland for example, even though the amount of time it takes to buy a property now is 7.5 months, and this has risen from 3.9 months pre-pandemic levels, the fallen through rate has fallen from 18.5% in 2019 to 15% today.

In the South West, the amount of time it takes to buy a property now is 5.5 months, and this has risen from 3.1 months pre-pandemic, the fallen through rate has fallen from 23.2% in 2019 to 20.7% today.

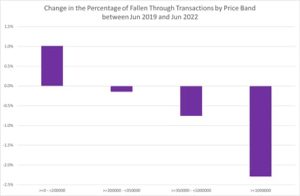

Finally, we turn our attention to price bands. The following chart displays the change in the percentage of fallen through transactions by price band between June 2019 and June 2022:

The above displays a large difference in the changes in fallen through rates. With the cheapest properties worth less than £200,000, which clearly shows an increase in the rate of fallen through sales. Here the fallen through rate in 2019 was 20.2% and this has now risen to 21.2%.

However, with properties over £1m, the fallen through rate in 2019 was 21.1% and this has now fallen to 18.8%. The £350,000 to £1m price bracket has also, seemingly, experienced a reduction in fallen throughs.

Managing Director of TwentyCi, Colin Bradshaw commented:

“Where people are buying medium to expensive properties, they are less likely to pull out of the transaction that they have commenced.

So, people who are starting out tend to be on lower incomes than people who buy more expensive properties, and as such, they are disproportionately affected by the squeeze on household incomes and the economic consequences of inflation.

However, the people that are buying properties that are less than £200k are clearly not affected as much.

But we all realise that a healthy property market can’t exist in the long run, without strong demand from first-time buyers. At the minute, the buyers are being replaced, the underlying demand is very strong (especially at the lower property prices as we have shown previously), but whoever the next Prime Minster is – Rishi or Liz – this is another one of the things they will have to consider.”

Join nearly 5,000 other conveyancers – sign up to our newsletter