Following the launch of the Centre for Finance, Innovation and Technology’s Open Property Roadmap, Leon Ifayemi, director of coalitions and research at CFIT, explains why conveyancers will play a crucial role in its delivery.

For most people, buying or selling a home remains one of the most stressful and uncertain transactions they will ever undertake. For conveyancers, it is a process defined by fragmented information, repeated verifications, rising compliance demands and persistent pressure to progress transactions within a system that remains heavily manual.

The scale of the challenge is well evidenced. Transactions take an average of 22 weeks to complete, around one in three fail before completion, and roughly 530,000 transactions collapse each year – creating around £560 million in wasted consumer costs and close to £1 billion in wider economic losses.

Yet perhaps the most striking finding from the first phase of CFIT’s Open Property Coalition is that less than 1% of the information required to buy a home is fully digitised.

This helps explain why conveyancers spend so much time collecting, checking and re-sharing information that often already exists elsewhere in the transaction chain. Property data, identity checks, source-of-funds verification, local authority information and transaction updates are typically spread across disconnected systems with limited interoperability.

As a result, conveyancers are the operational glue holding a fragmented, largely analogue, system together.

The challenge, therefore, is not simply digitisation, but trusted interoperability.

Transforming homebuying through Smart Data

Building this trusted interoperability is the focus of CFIT’s recently published Open Property Roadmap, commissioned by the Department of Business and Trade and developed through the UK’s first cross-sector Smart Data coalition of its kind beyond financial services.

The Roadmap explores how Smart Data principles – secure, consent-based and interoperable sharing of verified information – could transform the homebuying process while improving trust, transparency and efficiency.

For conveyancers, this is less about removing paperwork and more about rethinking how information is created, verified, shared and reused across a transaction lifecycle.

At the heart of this shift is the idea that value lies not only in digitising individual documents, but also allowing them to talk securely to one another, whether they are new or existing datasets.

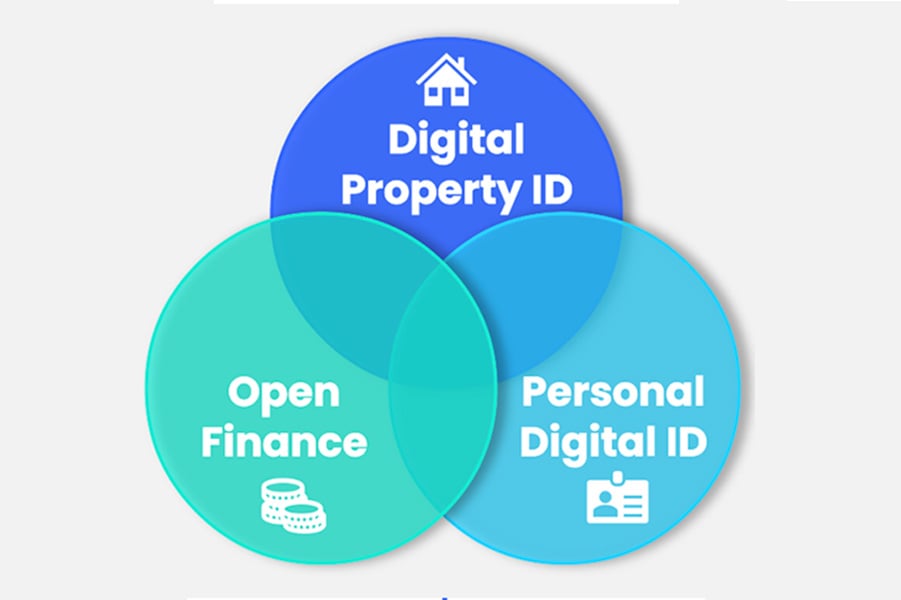

Beyond property: the digital property ID and Smart Data pack

One of the core concepts emerging from CFIT’s coalition is the digital property ID.

Rather than a static document, this would be a dynamic, reusable framework of verified information linked to a unique property reference number (UPRN). It could include ownership and title data, material information, planning history, risk indicators, transaction status and consent records.

But the opportunity goes further. A successful property transaction depends on three categories of data: property information, identity information, and financial or behavioural data. Together, these underpin conveyancing work across compliance, risk and legal verification.

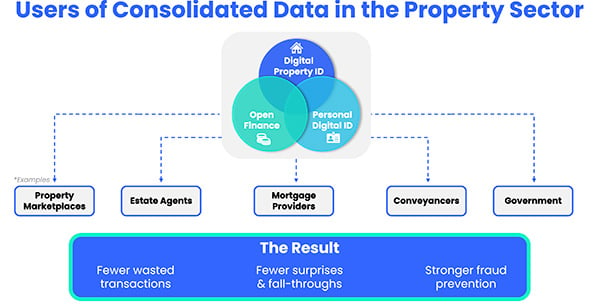

This points towards a broader concept – a Smart Data pack.

This would combine the verified property data, digital identity credentials and relevant financial information into a secure, reusable set of trusted data that can move across the transaction chain.

Instead of repeatedly requesting and verifying the same information, conveyancers and other actors could rely on pre-validated data, updated and shared through controlled permissions.

In practice, this could mean earlier confirmation of identity, faster source-of-funds verification, improved mortgage readiness insights and clearer transaction visibility. It would reduce duplication and allow conveyancers to focus more on legal judgement, risk management and client advice.

Ultimately, these efficiencies and improvements would accelerate the transaction process and mitigate the economic losses at the heart of this issue.

From conveyancer to digital transaction orchestrator

This shift has implications for the role of conveyancers themselves.

Today, conveyancers act as information gatherers, validators and coordinators across fragmented systems. Much of their time is spent chasing updates, reconciling data and managing friction created elsewhere in the process.

In a Smart Data-enabled environment, conveyancers have the opportunity to evolve into trusted orchestrators of transaction data.

Rather than simply consuming information, they could become stewards of verified data flows – helping ensure information is shared, updated and relied upon appropriately across parties.

Some firms may also play a role in maintaining elements of digital property IDs or managing secure exchange mechanisms for verified information.

This opens the door to a new category of conveyancer – firms that combine legal expertise with data stewardship, verification capability and transaction orchestration.

The opportunity is not just efficiency. It is a shift towards more strategic, trust-based roles within the property ecosystem.

Turning the roadmap into reality

However, our Roadmap is clear that implementation is not simply a technology challenge.

Questions of liability, consent, auditability, trust and reliance are fundamental. Who is accountable when data changes? How is consent managed and revoked? What constitutes sufficient assurance for reliance? How are trust events recorded?

These are not technical questions alone. They are legal and operational questions where conveyancers’ expertise is essential.

Importantly, many of the building blocks already exist: digital identity systems, Open Banking infrastructure, property datasets and emerging data standards. The challenge is not invention, but integration.

This is why the coalition has prioritised trust and interoperability frameworks alongside technical design, building on existing initiatives such as the Property Data Trust Framework, RICS standards, OSCRE and the wider government Smart Data agenda.

Phase 2 of the coalition will now proceed with the discovery phase, prototyping and implementation. This will explore interoperability models, governance frameworks, liability structures and Smart Data-enabled transaction flows.

Crucially, it will also test new operating models for and with conveyancers – as data stewards, trusted intermediaries and orchestrators within a more connected ecosystem.

Conveyancers will be key

Conveyancers will therefore be central to shaping what comes next.

This is fundamentally about creating a trusted, interoperable ecosystem where verified information can move securely between authorised participants with appropriate consent and legal certainty.

We have already seen through Open Banking how Smart Data can transform sectors when industry, regulators and government align around shared standards and outcomes.

The opportunity now is to apply those lessons to property – and to ensure the legal and conveyancing profession helps design the system it will ultimately operate within.

About the author

Leon Ifayemi is director of coalitions and research at the Centre for Finance, Innovation and Technology (CFIT). He leads the all-important design and implementation of CFIT’s coalitions, coalescing stakeholders in government, academia, industry and the third sector around key industry issues and driving forward the collaborative, strategic and research-led work of CFIT coalition partners. He sits on the board of Digital Leaders and is a former founder himself, with experience in private equity at Edmond de Rothschild. With a background spanning digital innovation, entrepreneurship, and financial services, he brings a wealth of diverse technical and creative expertise to CFIT. Underpinning Leon’s role is the idea of driving transformation: creating the conditions to inspire innovation and reshape a more inclusive financial ecosystem that benefits the full spectrum of consumers and SMEs.

One Response

Crucial questions about the reliability of ‘data’ and ‘liability’ keep being avoided. You can’t trust ‘data’ or information that has been generated by sellers themselves. You’re looking for information that may not be there – e.g. how many people get windows/doors/electrics installed and the tradeperson does not give them a certificate (I’ll give you a clue, a lot of them!) Doesn’t mean they weren’t done to standard.

You are also avoiding the questions of building safety and service charges. This data cannot be “trusted” as the information can change at the drop of a hat, the buildings that developers have built in the last 25 – 30 years have proven to be unsafe with lots of corners cut, Councils and Housing Associations as well as management companies may deliberately not provide information requested because they think they are right (e.g. where fire risk assessments are required).

You seem to be applying a solution that may work for 1:1 transactions but will not work where there are chains involving third party management companies.