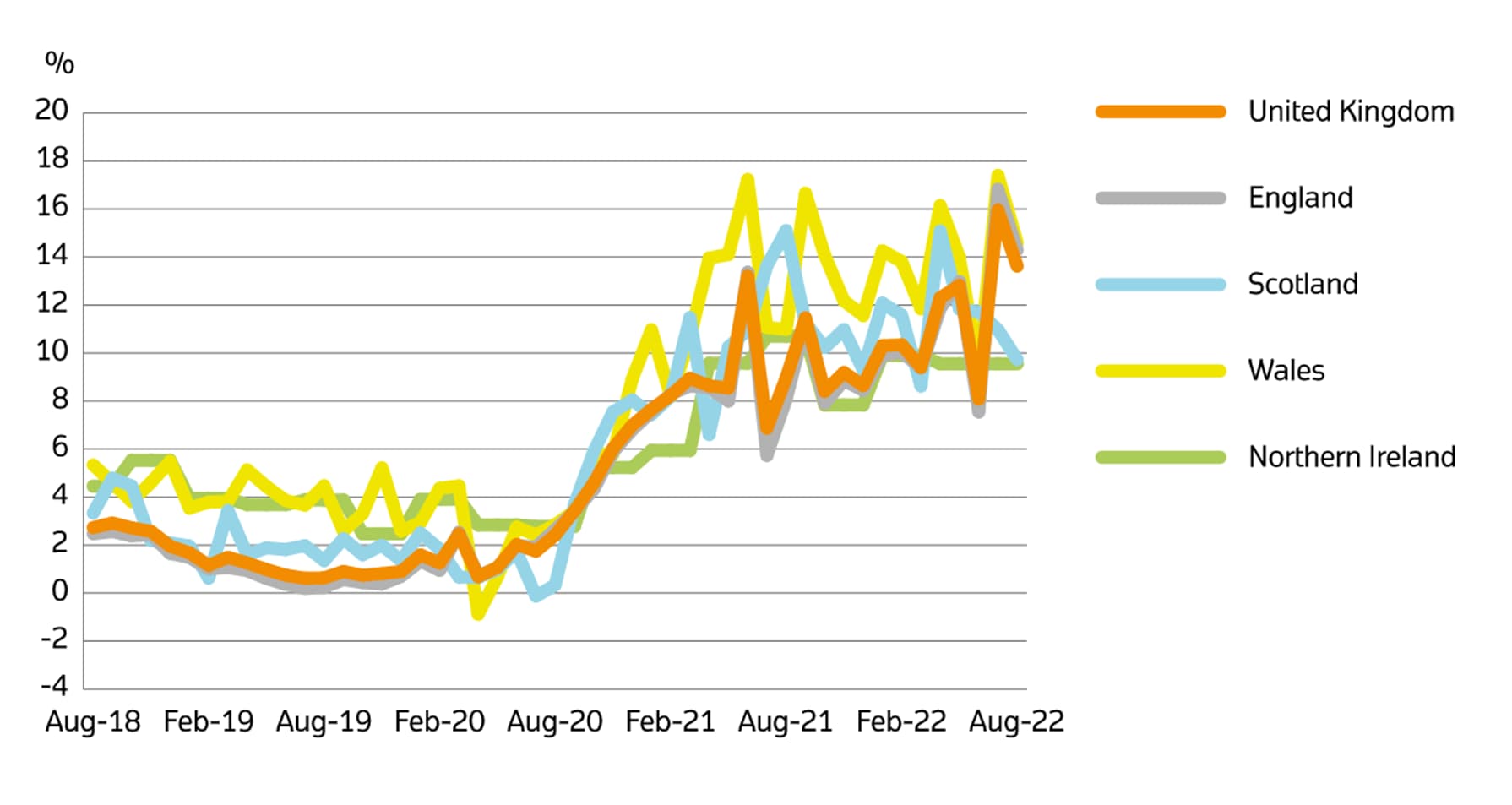

HM Land Registry (HMLR) has confirmed that house prices across the UK climbed a further 0.9% in August 2022 to an average of £295,903, totalling an annual price change of +13.6%.

House price growth was strongest in the South West where prices increased by 17.0% in the year to August 2022. The lowest annual growth was in London, where prices increased by 8.3% in the year to August 2022.

What’s next?

With current house prices a reflection of demand in May, new buyer demand is a better indication of where the market is headed. On this, RICS’ August 2022 UK Residential Market Survey reported that new buyer enquiries continue to decline, with supply on the market remaining restricted.

What’s more, data from Rightmove and Landmark Information Group seemed to corroborate RICS’ findings, with the latter describing a “fragmented property transactions pipeline”.

Propertymark also reported this week that the number of homes for sale per member estate agency branch is up 50% since April to 30, indicating people are still keen to get on the move – though this may put downward pressure on house prices.

Yet, with prices still climbing into August, the stamp duty cut still fresh in memory, and the Bank of England’s Agents summary of business conditions 2022 Q3 reporting that demand for property still exceeded supply, the picture is uncertain. Does the market really look like one on the precipice of catastrophe?

The industry’s reaction

Malcolm Webb, Technical Director at Legal & General Surveying Services, said:

“Today’s data confirms that house price growth remained resilient over the summer. However, it may be some time until we have the data to analyse the volatility felt by the UK housing market in the last few weeks. The fast-moving nature of today’s market also makes it extremely challenging to forecast which way house prices will go next.”

Andy Sommerville, Director at Search Acumen, said the last two weeks have shown “anything could change at the drop of a hat” and that homebuyers are not fans of such uncertainty:

“Today’s rise in house prices for August may be the last we see for some time as consumer confidence hits the breaks. We’ve seen Rightmove note overall buyer demand has slumped 15% compared with the same fortnight in 2021, indicative of a cold winter ahead.

If the new mood music from the Treasury can reassure global financial markets, this should ultimately reduce the ceiling on future increase rate rises from the Bank of England. But in comparison to the last decade, elevated mortgage rates are going to be a fact of life for the foreseeable future, which will inevitably impact supply and demand.

With mortgage offers at risk of being revised or withdrawn, there will be more pressure than ever on the wheels of the property transaction process to turn smoothly and swiftly to get transactions over the line.”

“August’s slowdown in house price growth will have been a slight relief for first-time buyers,” said Simon McCulloch, Chief Commercial & Growth Officer at Smoove, though he said this is not indicative of the full picture as of now:

“Fast forward to today and the recent political instability, alongside market volatility and high interest rates, means first-time buyer affordability is even more squeezed. It will be interesting to see if there is a further dip in next month’s figures. The stamp duty tax cut being maintained though should help provide some reassurance and encourage those who are still able to move to do so. A shortage of housing market stock will also continue to underpin house prices.”

James Forrester, Managing Director of Barrows and Forrester, was optimistic:

“The UK property market […] continues to move forward at pace despite the chaos that has unfolded across the wider economy.

A commitment to cutting stamp duty will certainly act as the cherry on the cake for many homebuyers, but it’s their continued ability to borrow in order to buy that will keep the cogs of the property market turning.

As it stands, they remain more than able, with the majority of lenders still offering a great level of products at what remain favourable rates. With stability now returning to the gilt markets, we can expect the mortgage sector to level out after what has been a rough few weeks and this will ensure the market remains in good health over the coming months.”