The resilience of the housing market in the face of affordability challenges and an uncertain economic backdrop is set to continue, according to Halifax’s head of mortgages.

Commenting on the release of the Halifax House Price Index for May, Amanda Bryden said the market appears to have absorbed the surge in activity driven by changes to stamp duty and remains largely stable.

She added:

“Affordability remains a challenge, with house prices still high relative to incomes. However, lower mortgage rates and steady wage growth have helped support buyer confidence.

“The outlook will depend on the pace of cuts to interest rates, as well as the strength of future income growth and broader inflation trends. Despite ongoing pressure on household finances and a still uncertain economic backdrop, the housing market has shown resilience – a story we expect to continue in the months ahead.”

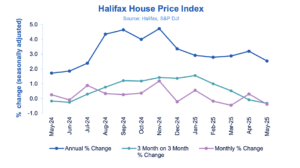

House prices fell by 0.4% in May after rising by 0.3% in April, taking the average property price to £296,648. However, there remains a significant regional variation in growth, with Northern Ireland, Wales and Scotland outpacing English regions.

Northern Ireland once again recorded the fastest pace of annual property price inflation, up by 8.6% over the past year. The typical home now costs £209,388, though prices remain well below the UK average. Wales and Scotland also posted strong annual growth of 4.8% in May, taking average prices to £230,405 and £214,864 respectively.

Among the English regions, the North West and Yorkshire and the Humber showed strongest growth. With both regions up 3.7%, average values are now £240,823 and £213,983 respectively. London continues to see more subdued growth, with prices rising by just +1.2% year-on-year. However, the capital remains by far the most expensive part of the UK housing market, with the average home now priced at £542,017.

Anthony Codling, managing director of equity research at RBC Capital Markets, welcomed the figures. He commented:

“The Halifax reported today that house prices fell by 0.4% in May, whereas on Monday Nationwide reported house prices were up 0.5% – we think therefore the best conclusion is that house prices are stable. Stable house prices are the happy medium not pushing prices further out of reach for homebuyers, whilst not reducing the wealth of those already on the housing ladder. As we start to move into summer and thoughts turn to summer holidays, activity in the housing market typically slows. Therefore, stable house prices is a welcome state of affairs reducing the fears of missing out for buyers or concerns of negative equity for owners.”

Iain McKenzie, CEO of The Guild of Property Professionals, agreed the figures are encouraging and said they offer a positive outlook for buyers:

“Following the anticipated recalibration in April after the March stamp duty rush, it’s encouraging to see how resilient prices have been. A minor dip of this scale was widely predicted, and the fact that it wasn’t more significant is a testament to the market’s firm footing.

“This resilience is underpinned by a confluence of positive factors, such as the recent welcome interest rate cut, providing a tangible boost to borrowers, and robust economic fundamentals. The stronger-than-expected 0.7% GDP growth in Q1 certainly paints a more optimistic backdrop.

“While the recent uptick in inflation has tempered expectations for further rapid rate cuts, the key fundamentals supporting homebuyers remain strong – low unemployment, rising real earnings, and the continued anticipation of easing borrowing costs in the medium term.”

“Crucially, the market’s overall stability is fostering buyer confidence. With reports, like Zoopla’s, indicating that a very high percentage of homes are still achieving their asking price, it’s clear that buyer motivation is strong. This marginal price adjustment, when viewed alongside these supportive conditions, reinforces our positive outlook for the housing market as we move through 2025.”