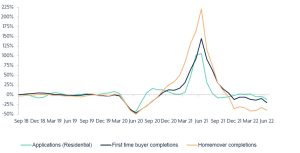

The UK Household Finance Review for the second quarter has been released. According to the review, house purchase activity is reverting back to pre-Covid levels with Q2 of 2019 and this year showing similar results.

Figures show that homeowners completions were down almost 250% compared to this time last year. This is as expected due to consumers rushing to complete purchases in Q2 2021 to complete purchases before the end of the second phase of the Stamp Duty holiday. The review suggests completions have now returned to pre-Covid levels.

These findings correlate with the findings in the recently published Nationwide HPI where it was found surveyors reported fewer new buyer enquiries. However, the findings differ on the number of mortgage approvals where the Nationwide HPI recorded mortgage approvals had fallen below pre-pandemic levels, although only modestly.

In addition to this, the total number of customers in arrears on their mortgage continued to fall, the fifth quarter of successive decline. However, the review also expects there to be an increase in the number of people going into arrears in the coming months due to the cost of living crisis and rising inflation.

The number of borrowers in larger arrears (10% or more of the mortgage balance) were found to have fallen for the second successive quarter. However, those with arrears representing between 2.5 and 5% of the balance was shown to have risen slightly by 170 cases to 25,160.

The number of possessions remained unchanged from Q1 figures, which was attributed to delays in court cases from the backlog in the courts. As such, the review predicted possessions to increase throughout the year as the courts work through the delayed repossessions.

Findings also suggested that those seeking a mortgage will find more limited options. This is also blamed on rising Bank of England interest rates and a rising cost of living. The report also stated:

“This suggests that a significant proportion of borrowers would find their refinancing options constrained on the open market.

The same affordability pressures are likely to bear down on effective demand for new house purchase mortgages as we move through this year and beyond, whilst inflation outpaces wage growth.

The report added that house purchase activity looks to have returned to pre-pandemic norms for now but warned of headwinds from cost-of-living pressures, which could hit demand.”

Vikki Jefferies, Proposition Director, PRIMIS, commented:

“Although borrowing has dropped for house purchases, we expect remortgage and buy-to-let activity to remain buoyant for the rest of the year.

With today’s data showing elevated pressures on household budgets, advisers can support consumers by offering a range of flexible products that will enable them to maximise their assets to enhance their finances in the long-term.

However, given approximately £100bn of mortgages are set to mature by the end of 2022, brokers will have an extremely busy pipeline of business in the coming months, and they will certainly be stretched. It will be vital to provide them with proactive and sustained support, and as such, we will continue to support our brokers through our Virtual Experts page and our product desk will be on hand to assist with client queries.”

Read the full UK Household Finance Review here.

Join nearly 5,000 other conveyancers – sign up to our newsletter