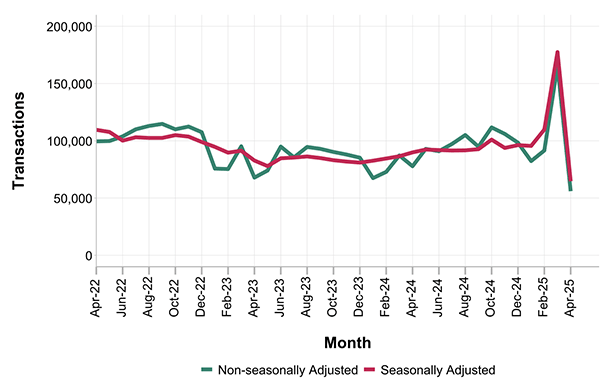

Property industry experts continue to be optimistic about the housing market, despite the latest UK monthly property transaction data showing a steep decline. HMRC’s non-seasonally adjusted residential transactions decreased by 66% in April 2025 relative to March 2025 – the highest month-on-month decrease since records began for non-seasonally adjusted figures.

The provisional seasonally adjusted estimate is 64,680, 28% lower than April 2024 and 64% lower than March 2025. For non-residential transactions, the figure is 9% lower than April 2024 and 16% lower than March 2025, at 9,410.

‘The April transaction figures from HMRC are, on the surface, quite stark, but they absolutely need to be seen in the context of the unprecedented rush to beat the March Stamp Duty deadline’, Iain McKenzie, CEO of The Guild of Property Professionals, said.

“A cooling off period was inevitable after such a surge, which saw activity brought forward. What’s more encouraging are the underlying trends: the recent Bank Rate cut to 4.25%, consistently falling mortgage rates, with sub-4% deals now more accessible for many, and lenders showing increased flexibility. These factors are easing some affordability pressures.”

Andrew Lloyd, managing director at Search Acumen, said demand is still strong and pointed to a stronger performance in the commercial sector. He commented:

“Across the market we are still seeing a strong appetite for deal flow and a demand for bricks and mortar that will continue to resonate throughout the upcoming months.

“Residential is only one part of the full picture. In commercial property, a combination of rental growth, yield impact turning positive, and looser credit constraints contributed to an impressive performance led by the retail sector.”

However, Joe Pepper, UK chief executive office at PEXA, questioned whether the decline could be due to an inefficient home buying process causing sales that missed the deadline for the Stamp Duty changes to fall through, and said digital transformation should be seen as a priority.

He added:

“Even with the rush for buyers to beat the Stamp Duty deadline, April’s figures have not shown an increase in transactions. Whether this is because some transactions fell through as a result of having to pay more tax or something else entirely, it is sadly an indication that the transaction process is not as efficient as it needs to be.

“This is not the fault of conveyancers or other stakeholders – they are working as fast as possible to deliver good consumer outcomes which has always been a key focus…The existing infrastructure is creaking at the seams, and with a government putting the housing market at the centre of its economic growth plans the urgency of investment in vital digital transformation to support scalability cannot be overstated.”

Looking ahead, Zoopla’s executive director Richard Donnell said the company’s own data supports resurgence.

He explained:

“Our latest data shows a lull in new sales over Easter but a significant pick-up in sales agreed in recent weeks, reaching their fastest pace in four years. This resurgence is supported by less stringent affordability testing for mortgages, a larger pool of active buyers and an increase in homes available for sale. We anticipate this momentum will lead to 1.15 million sales in 2025, a 5% increase from 2024″

Finance professionals were similarly upbeat. Karen Noye, mortgage expert at Quilter, said:

“History tells us that when temporary tax reliefs drive the market, they often create frenzied spikes followed by sharp slowdowns. We saw this during the pandemic, and today’s figures are just another reminder that short-term incentives don’t guarantee long-term stability.

“However, don’t write off the market just yet. With the Bank of England trimming interest rates to 4.25%, mortgage rates have been drifting lower, with sub-4% deals becoming more common. As cheaper fixed-rate mortgages and lower reversion rates take hold, buyers emerging from their current deals could find the conditions much more favourable.”

And Simon Webb, managing director of capital markets and finance at LiveMore, said the outlook remains ‘encouraging’, particularly amongst older buyers. He added:

“With interest rates expected to fall further this year, confidence is gradually returning and we believe the later life lending market will continue to grow in importance – not just as a source of housing activity, but as a key enabler of financial wellbeing in later life. The challenge now is to ensure that lending criteria, product innovation and advice services continue to keep pace with changing customer needs.”

See the full transaction data at https://www.gov.uk/government/statistics/monthly-property-transactions-completed-in-the-uk-with-value-40000-or-above/uk-monthly-property-transactions-commentary–2

2 responses

David Jabbari, CEO Muve. This is totally explained by the “pull forward” of completions into March. The underlying market is extremely strong, and above pre-Covid averages. A non-story!

This is a perfect example of heard mentality, not one person sees risk its all “positive”. Interest at ~4% is still for the majority of people in this country an extraordinary amount of their wage gone each month and alot of households have not yet moved from their low rate mortages thats going to come this year and next [5 year fixes ending], houses above £350k are not selling, prices are consistently being reduced just follow rightmove listing’s… at the £450k the stamp duty tax starts to becomes eye watering that most people even if they could afford it, will not contemplate shelling out £12k+ for old rope if the home theyre living in is perfectly fine.

I’d be willing bet you see a stamp duty policy reversal in 2026/27 as the housing markets tanks for most places outside of London in 4Q of this year if nothing but to stimulate tax receipts that are not forthcoming.