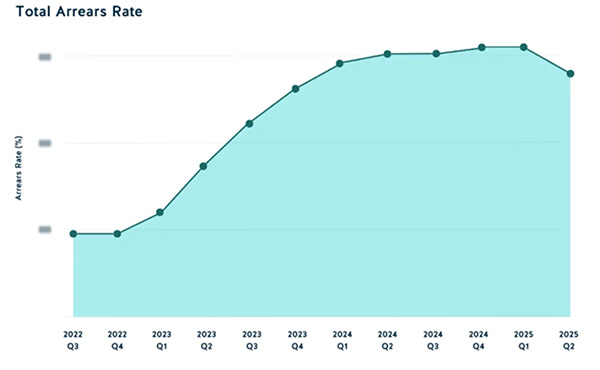

Mortgage arrears are down across all regions of the UK* for the first time since the cost-of-living crisis began, according to data from global credit intelligence company Pepper Advantage.

Overall UK arrears, which include residential and buy-to-let mortgages, dropped by 4.4% in Q2 2025 compared to the previous quarter – the first widespread improvement since the second quarter of 2021. Residential arrears fell by 4.7% and direct debit rejections fell by 5.1%, marking the first quarter that both metrics have fallen since the Covid pandemic.

The data – gathered from Pepper Advantage’s portfolio of over 100,000 residential mortgages – suggests affordability challenges are improving, the company said.

Managing director Aaron Milburn commented:

“The significant drop in residential mortgage arrears, alongside the simultaneous decline across all UK regions, is a promising sign that some household financial pressures may be easing after years of inflation and rising living costs This marks the most positive quarterly movement we have observed since this report began.”

Arrears rates fell across every UK region for the first time since Q2 2021, indicating a UK-wide easing of financial pressure after years of inflation and rising living costs. The largest improvements were seen in the North West (-7.9%), Wales (-7.7%), and East Midlands (-7.0%), while London (-0.9%) and the South East (-3.1%) posted the smallest declines.

‘The universality of the drop in arrears across our portfolio indicates that UK household budgets are benefiting from less acute inflationary pressures and lower interest rates’, the report notes.

However, the company warned that any recovery remains fragile, adding:

“It is important, despite this positive momentum, to recognise the potential challenges that lie ahead. With inflationary pressures and possible tax increases on the horizon, there is a risk that household budgets could come under renewed strain.

“These factors may lead to a reversal of the progress made in arrears in the first half of 2025, and we remain cautious as we continue to monitor the health of our UK portfolio.”

*Excluding Northern Ireland due to sample size.