Downwards trends in the property market show signs of stabilising, according to the latest sentiment survey from the Royal Institution of Chartered Surveyors (RICS).

According to RICS members, the negative trend remains, with fewer enquiries and sales, but market evidence suggests “the pace of deterioration is no longer intensifying”.

The supply of housing to the market continues to slow, with survey responses showing a net balance of -8% in May, a slightly more negative figure compared with April. Market appraisals also show a weaker market than 12 months ago, with the net balance of -16% suggesting the near-term pipeline for new listings may remain constrained.

New buyer enquiries recorded a net balance of -34% in May, unchanged from the previous month. While this continues to show weaker demand, it is the first time since the start of the year the figure has not fallen further, suggesting a stabilising of momentum.

Agreed sales also remained subdued, posting an unchanged net balance of -37% which again shows completions continue to fall but suggests the continued slide has come to a halt.

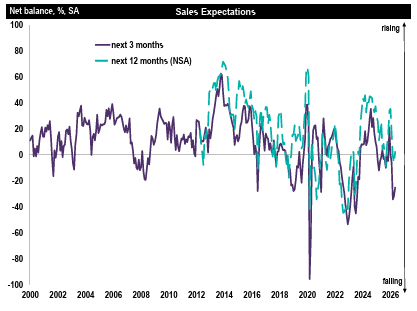

Source: RICS UK Residential Market Survey

Near-term sales expectations have improved slightly to -25%, compared with readings of -32% and -34% in the previous two reports. Over a 12-month horizon, sales expectations moved into neutral territory at +2%.

Members also report the time to complete is now at its longest duration since RICS began measuring the sentiment in 2017: an estimated 21.5 weeks nationally.

Tarrant Parsons, RICS head of market research and analysis, said: “The latest survey data suggest the recent downturn in activity may be beginning to stabilise, with several key indicators broadly holding steady. However, as they remain in negative territory, it would be premature to interpret this as the start of a recovery.

“The decline in CPI inflation to 2.8% in April provided some temporary relief, but the Bank of England has signalled that further inflationary pressures are likely as higher energy costs continue to pass through. Against this backdrop, the prospect of further rate rises cannot be dismissed, and until there is greater clarity, market sentiment is likely to remain fragile.”