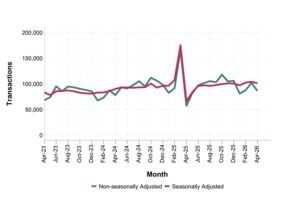

Property transaction trends are broadly in line with expectations, after the latest HMRC residential transaction numbers revealed a seasonally adjusted estimate of 101,030 transactions in April, 3% lower than last month.

While the impact of the Middle East conflict continues to play a part in inflation and consumer confidence, there is still “strong intent” amongst households to move home, according to Richard Donnell. The executive director of Zoopla said: “April saw a 3% fall in completed home sales versus March which is in line with previous years as households rush to complete sales before Easter each year.

“Overall, housing sales in April were running 3% ahead of the previous 12 months as the number of housing sales increased from the low of 2023 when activity was hit by higher mortgage rates. We expect housing sales to end 2026 at close to 1.2 million – the 20 year average and a healthy position given the impact of higher mortgage rates and economic uncertainty.”

Jason Tebb, president of OnTheMarket, said the slight dip suggests consistent resilience from the housing market in the face of economic and political uncertainty.

“Rather than stepping back and delaying decisions, buyers and sellers are mostly adapting to change and continuing to progress with their transactions,” he explained.

“The steady interest rate environment, with the Bank of England holding rates at recent meetings, suggests a welcome calm and considered approach while inflation is monitored. At the same time, lenders continue to trim their mortgage pricing, which is helping ease affordability and is particularly welcome as the cost of living remains high.

“Sellers have plenty of choice with more stock coming to the market, which is putting them in a strong negotiating position. This is helping keep property prices in check, which should also assist in improving transaction numbers.”

April’s figures are 53% higher than the same period last year, but Anthony Codling, managing director of Equity Research at RBC Capital Markets, pointed out comparisons to 12 months ago are unhelpful.

“Last April saw just 65,960 transactions as buyers vanished following the March 2025 SDLT deadline, when completions surged to 175,180. Strip away the distortion and you’re left with transactions down 3% month on month and running just 2% above the five year and 10-year averages – hardly a housing market on fire.

“These figures tell us what was happening 8-12 weeks ago when offers were made, not what’s happening now. With mortgage rates still elevated and consumer confidence fragile, the real test lies ahead in June and July data. For house builders, April’s numbers confirm we’re in a holding pattern, not a recovery.”

Nathan Emerson, CEO of Propertymark, offered a balanced view but warned there could be trouble ahead. He said: “While it is disappointing to see the volume of non-seasonally adjusted housing transactions display negativity month-on-month, when viewing the wider picture year-on-year, they show a return to more expected numbers, all following changes to thresholds to stamp duty at the start of April 2025.

“Sentiment within the housing sector remains a central indicator of economic health. With global unease continuing to add potential unforeseen pressures for many people, it is important to apply a sense of caution regarding affordability over the coming weeks and months.

“We have recently witnessed Ofgem raise the energy price cap by 13%, effective from July. This, coupled with what is a generally changeable direction for both inflation and base rate, could add up to producing a challenging period ahead.”

It’s a sentiment echoed by Andrew Lloyd, managing director at property data firm Search Acumen, who said the transaction data reveals the extent of the challenges facing the property market and the wider economy.

“Any thought that we were already past the worst of it has proven misplaced,” he explained.

“Given the greater vulnerability of the residential property market, where hesitation on the part of one buyer and seller can snap a much longer chain of transactions, it is no great surprise to see a dip in residential transactions in the face of substantial house price uncertainty. As the UK bakes under a summer sun, we have had no real spring bounce to talk of.

“What’s ahead for the property market is likely a flattening of transaction volumes, balancing the underlying market swings of supply and demand that keep it steady, against a trend of deals falling out of bed as prices and affordability remain unclear. Data might start to show a spike in smaller landlords continuing to sell up after the combination of tax and regulatory shocks following the Renters Rights Act. Consequently, we’re likely to see more corporate landlords taking their place.

“If it was possible to meaningfully move faster, we may well have seen even more transactions over the last month to beat any potential interest rate hikes that could be coming our way. But sticky markets mean more deals are falling out of bed – we know more than half of residential property transactions in the UK fall through after an offer has been accepted.

“This is not just heartache for movers, but significantly economically damaging as the UK paddles furiously against broader headwinds. We are watching AI investment boom, so it makes sense that the use of technology and data standardisation across the property transaction chain must become the norm if we want to reduce risk and accelerate growth. Otherwise, we can expect to see this engine continue to cough and splutter more often than it should.”

With the output of the government’s home buying and selling consultation expected imminently, systemic change can’t come quick enough for Maria Harris, chair of the Open Property Data Association.

“While transaction levels remain under pressure, the more telling issue is the pace at which the system operates,” she said. “With the average completion taking around 17 weeks, the home moving process continues to be too slow and complex for the needs of today’s consumers.

“What we are seeing is not just a cyclical slowdown, but the impact of an outdated system struggling to support a modern housing market. We need to accelerate the shift towards a more digital, data-driven home buying process – one that improves speed, certainty and trust for consumers.

“We eagerly await the outcomes of the Ministry of Housing, Communities and Local Government consultation, which has recognised many of these challenges. The publication of its findings is an important next step in defining how the market can be reformed.”