New lending figures released by the Bank of England (BoE) this week have revealed a “significant drop” in mortgage lending to individuals. However, with mortgage approvals soaring, commentators have suggested the stats paint a “mixed picture” for the housing market.

Mortgage lending to individuals fell from a net flow of £0.7 billion in February to net zero in March. Looking at the period prior to the onset of Covid-19 in March 2020, this is the lowest level of net borrowing since June 2011. While gross lending increased slightly from £20.4 billion in February to £20.6 billion in March, gross repayments fell from £19.9 billion to £19.3 billion.

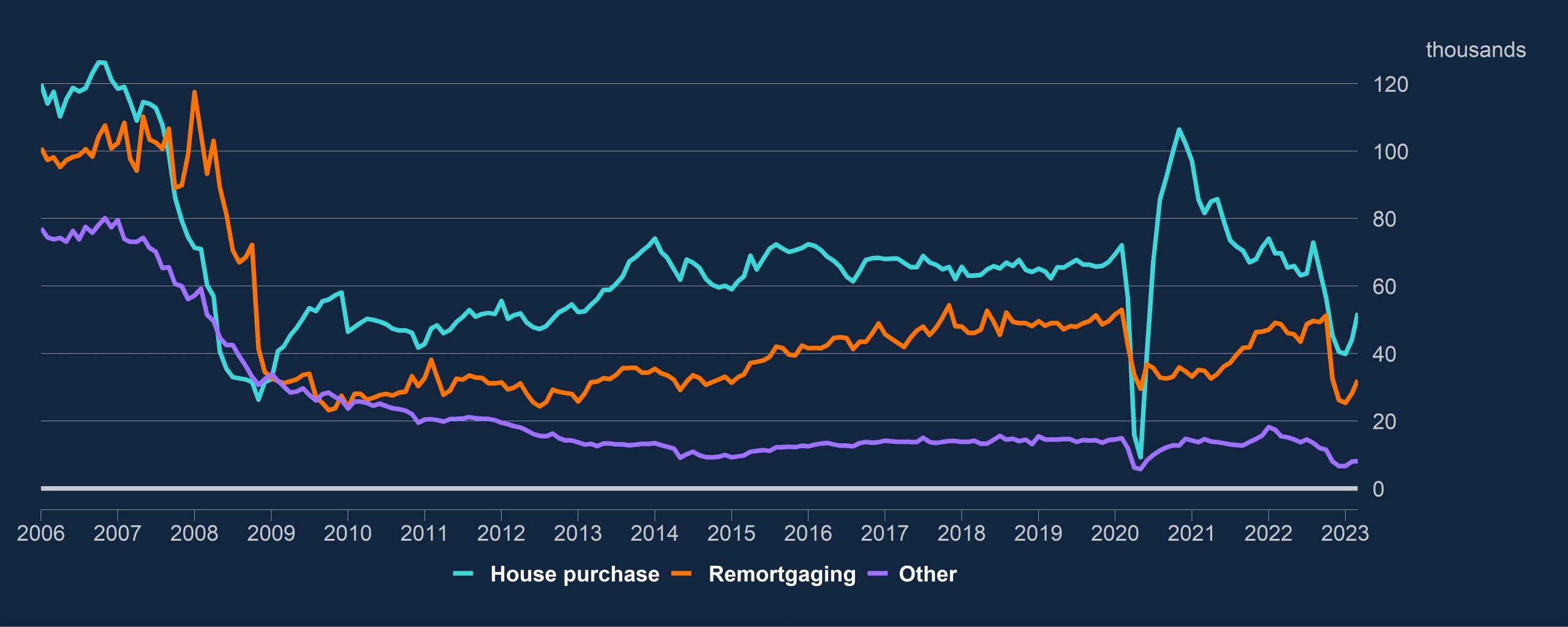

Despite this, figures for mortgage approvals – an indicator of future borrowing – appear to be more positive. Specifically, net mortgage approvals for house purchases rose to 52,000 in March from 44,100 in February.

This does, however, remain below the monthly average of 62,700 approvals seen throughout 2022. What’s more, recent data provided by Twenty7tec revealed purchase and remortgage searches via their platform fell by 18.3% and 25.4% respectively between March and April.

“Easter 2023 had a major impact on mortgage search volumes,” said Nathan Reilly, director at Twenty7tec, suggesting May could see a similar trend, in part down to the three bank holidays during the month.

Charlotte Nixon, mortgage expert at Quilter, said the figures released by Threadneedle Street “paint a mixed picture for the housing market”. On mortgage lending to individuals during the month, she said:

“This decline will be down to persistently high inflation, the elevated cost of living, and rising interest rates, which have placed considerable strain on household budgets.”

Commenting on the rise in mortgage approvals, Nixon said:

“This increase could be linked to a modest rise in consumer confidence, as individuals grow accustomed to mortgage rates around 4.5% and a predicted path to a base rate peak of 5%. This is also likely a result of the usual uptick in house purchases in spring.

However, with a base rate hike likely on the cards next week, this newfound optimism for buyers might be quickly dampened. Whether these increases are enough to completely rain on a usually more buoyant market in the spring and summer months is yet to be seen.”

Adam Oldfield, chief revenue officer at Phoebus Software, offered an optimistic appraisal:

“The increase in approvals for house purchases was substantial and the best sign yet that the housing market has turned a corner. Add to that the latest report that house prices increased in April and the picture is significantly better than we may have hoped a couple of months ago.”

He did, however, add the caveat that rising mortgage rates “will still be weighing heavy for many”, potentially reducing the number of buyers “willing to take the plunge”.

Sarah Coles, head of personal finance, Hargreaves Lansdown, suggested that onlookers shouldn’t read too much into two consecutive monthly rises in mortgage approvals given the deficit to long-term trends, though did comment that it is “adding fuel to the fires of optimism being lit across the property market” on the back of both Zoopla and Nationwide reporting house price increases in April. Coles concluded:

“The growth in mortgage approvals is due in no small part to falling mortgage rates – which have been creeping south since the peak in October last year. They’re still significantly higher than before the rate rises kicked off, and the falls took a break in March after the surprise inflation bump, so the effective interest rate on new mortgages was up 17 basis points to 4.41% in the month. However, they’ve started falling again, and we expect them to continue to drop through 2023. There has also been a small rally in sentiment. The GfK confidence index shows that people’s confidence in their own finances has picked up slightly over the past three months.

There are still headwinds, with inflation still horribly high and worryingly sticky – alongside growing concerns about a global slowdown and possible stagnation. However, there are plenty of people who are hoping the UK can avoid a recession this year, and that jobs could prove reasonably resilient – protecting those with mortgages to pay. There’s also the optimism that falling inflation later this year could help ease the pressure. None of those things are guaranteed to happen, but for the property market right now, it’s enough that people believe they might.”