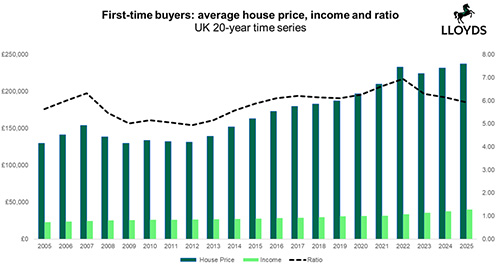

The average first-time buyer home now costs 5.9 times average earnings, the lowest ratio since 2015, according to the latest affordability review from Lloyds.

Research from the high street lender has found a combination of lower interest rates, higher incomes and limited property price growth has improved first-time buyer affordability over the last year, taking it to its most favourable level in a decade.

The typical first-time buyer property price is now a national average of £237,518, an increase of 2.4% over the last year. At the same time, average incomes have increased by 6.2%, to £40,021.

Typical monthly mortgage costs have risen by just 0.1% for first-time buyers over the last year thanks to lower interest rates, with the average monthly mortgage payment now £1,087 – 32% of the average monthly income.

“Buying your first home is still a big challenge, but things are moving in the right direction”, said Amanda Bryden, head of mortgages at Lloyds.

“Lower mortgage rates, stronger wages and slower house price growth mean it’s becoming a little easier to get on the ladder – the best it’s been for several years.”

Although average figures will not reflect reality in many areas, with Lloyds’ research finding significant regional variations, affordability has improved in almost every region of the UK.

In England, Greater London (9.3), the South East (7.3), Eastern England (7.0) and the South West (6.2) saw the biggest improvement in the property price to income ratio for first-time buyers over the last year, falling by 0.4 in each case.

While the North East of England remains the most affordable region for first-time buyers, with a property price to earnings ratio of 3.9, the figure reflects a slight increase from last year’s 3.8, with a property price increase of 10% outpacing the national average of 7%.

Mortgage costs as a percentage of income have remained static in the North East, at 22%, compared to 51% in Greater London.

In Wales, the property price to income fell slightly to 5.3, down 0.1 from last year. In Northern Ireland, the ratio stands at 5.1, up 0.2, while in Scotland the ratio remains unchanged at 4.0.

Calculations are based on typical first-time buyer property prices and the average interest rate for a five-year fixed deal – with a 30-year term and 10% deposit – which has fallen from 4.7% to 4.5% over the last year.

Commenting on the figures, Propertymark’s president Mary-Lou Press said:

“While it is encouraging to witness an emerging trend of falling rates on offer across many key mortgage products, as well as rising wages which are helping to enhance first-time buyer affordability, the autumn budget seemed like a missed opportunity in many ways to further energise the housing market overall.

“With a population expected to exceed 70 million people in less than five years, there is vast pressure to deliver new homes across all regions. Over the forthcoming year it will prove essential to see investment in the correct skillset and supply chains to enable this objective to become a reality.”

| Regional breakdown: First-time buyer affordability – Q3 2025 | ||||||

| Region | Property price | Income | Price to income ratio | Monthly mortgage | Mortgage % income | Monthly rent |

| Eastern England | £275,323 | £39,603 | 7.0 | £1,260 | 38.2% | £1,242 |

| East Midlands | £201,390 | £36,544 | 5.5 | £922 | 30.3% | £888 |

| Greater London | £467,924 | £50,152 | 9.3 | £2,141 | 51.2% | £2,252 |

| North East | £141,228 | £35,902 | 3.9 | £874 | 27.9% | £856 |

| North West | £197,088 | £38,121 | 5.2 | £646 | 21.6% | £741 |

| Northern Ireland | £190,926 | £37,618 | 5.1 | £902 | 28.4% | £914 |

| Scotland | £161,069 | £40,645 | 4.0 | £737 | 21.8% | £1,001 |

| South East | £304,075 | £41,396 | 7.3 | £1,392 | 40.3% | £1,382 |

| South West | £240,783 | £38,548 | 6.2 | £1,102 | 34.3% | £1,188 |

| Wales | £197,688 | £37,095 | 5.3 | £905 | 29.3% | £809 |

| West Midlands | £213,295 | £38,270 | 5.6 | £976 | 30.6% | £934 |

| Yorkshire & the Humber | £172,990 | £36,930 | 4.7 | £792 | 25.7% | £824 |

| UK average | £237,518 | £40,021 | 5.9 | £1,087 | 32.6% | £1,346 |

Source: Lloyds Banking Group, ONS