Despite the economy throwing almost every imaginable obstacle in the direction of the housing market, it seems that, as of July, the market is refusing to be beaten.

Indeed, HM Land Registry’s (HMLR) latest house price index shows a defiant market wherein prices climbed 2% in July on a non-seasonally adjusted basis, having grown by 1% in June.

Indeed, RICS’ July 2022 Residential Market Survey reported that new buyer enquiries were falling, yet a lack of stock, a steady mortgage market, and the underlying stoicism of British bricks and mortar seem to be propelling the market forward against all odds.

As such, the average price of a property in the UK has risen to £292,118, and the annual change in price for a property is a striking 15.5%.

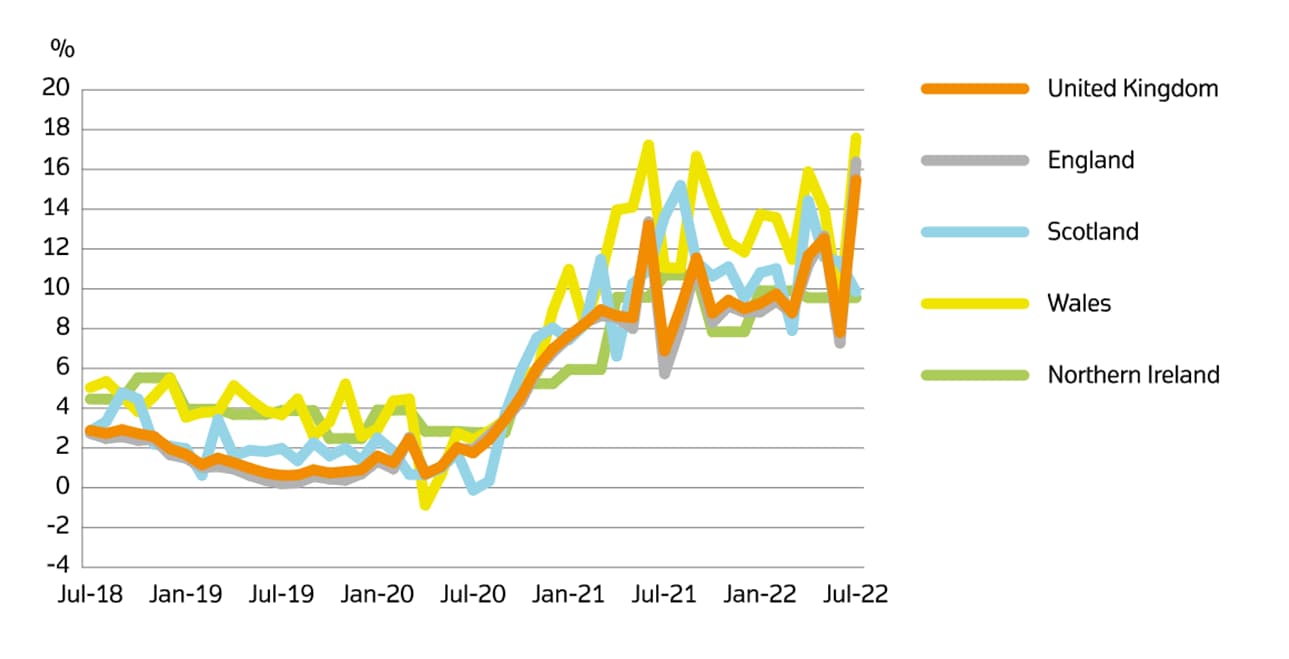

Annual house price change per country over the last five years

There is a general feeling that a downturn is inevitable at some point – that the market cannot withstand rampant inflation and rising interest rates forever, as well as a cost of living crisis which will increasingly impact demand.

Yet, the signs indicate that such a downturn is not imminent – in July, transactions soared, mortgage approvals rose, and house prices climbed. For now, conveyancers will remain as busy as ever.

Industry reaction

Simon McCulloch, Chief Commercial & Growth Officer at Smoove, said:

“July’s figures demonstrate the underlying strength of the UK housing market. While the cost of living crisis and associated Bank of England interest rate hikes continues to impact activity, the new administration’s decision to cap energy bills until 2024 will likely boost confidence, particularly around affordability criteria. The dynamics of the UK property market continue to be determined to some extent by a lack of supply, which should prop up prices to a degree even in the event of a prolonged recession.”

Founding Director of Revolution Brokers, Almas Uddin, commented:

“While homebuyers have been handed a momentary reprieve by the Bank of England, it’s almost certain that we will see yet another increase in interest rates next week.

Apart from the cost of our energy bills, mortgage costs have seen the second largest annual increase of all household outgoings and this cost is only going to increase further as lenders react to another hike to the base rate.

Of course, it’s important to note that they remain relatively low when compared to historic peaks and we are yet to see any decline in house prices as it stands. However, this increasing cost will put further strain on our household finances at a time when they are already stretched to breaking point.

As a result, we can expect those buyers entering the market with the help of a mortgage to do so in a far more conservative manner than they have been doing in the last few years. The result of this heightened caution is likely to be a slow in the high rates of house price growth seen since the pandemic.”

James Forrester, Managing Director of Barrows and Forrester, said:

“With the nation in mourning over the death of our longest reigning monarch, it’s fair to say that an increase in bricks and mortar value is probably the last thing on the mind of the nation’s homeowners at present.

But while we find ourselves in a week-long limbo until the state funeral next week, it’s the appointment of our new prime minister that is due to have a more significant influence on the housing market going forward.

With the cost of living crisis putting immense pressure on our household finances, failure to act is likely to see the huge levels of market momentum built since the start of the pandemic start to dissipate over the coming months.”

Managing Director of HBB Solutions, Chris Hodgkinson, added:

“The increasing cost of borrowing, coupled with the spiralling cost of running our homes, is already starting to dampen property market activity. So while topline house prices remain robust, it’s only a matter of time before this dwindling market sentiment starts to show and we see a decline in the rate of house price growth.

Those currently considering a sale are best advised to do so quickly, as sitting tight until next year could see them achieve a lower price for their home compared to current market conditions.”

Join nearly 5,000 other conveyancers – sign up to our newsletter